Alternative Data: A Risk Management or Revenue Tool?

Amy Hou | April 4, 2019 | Credit & Lending

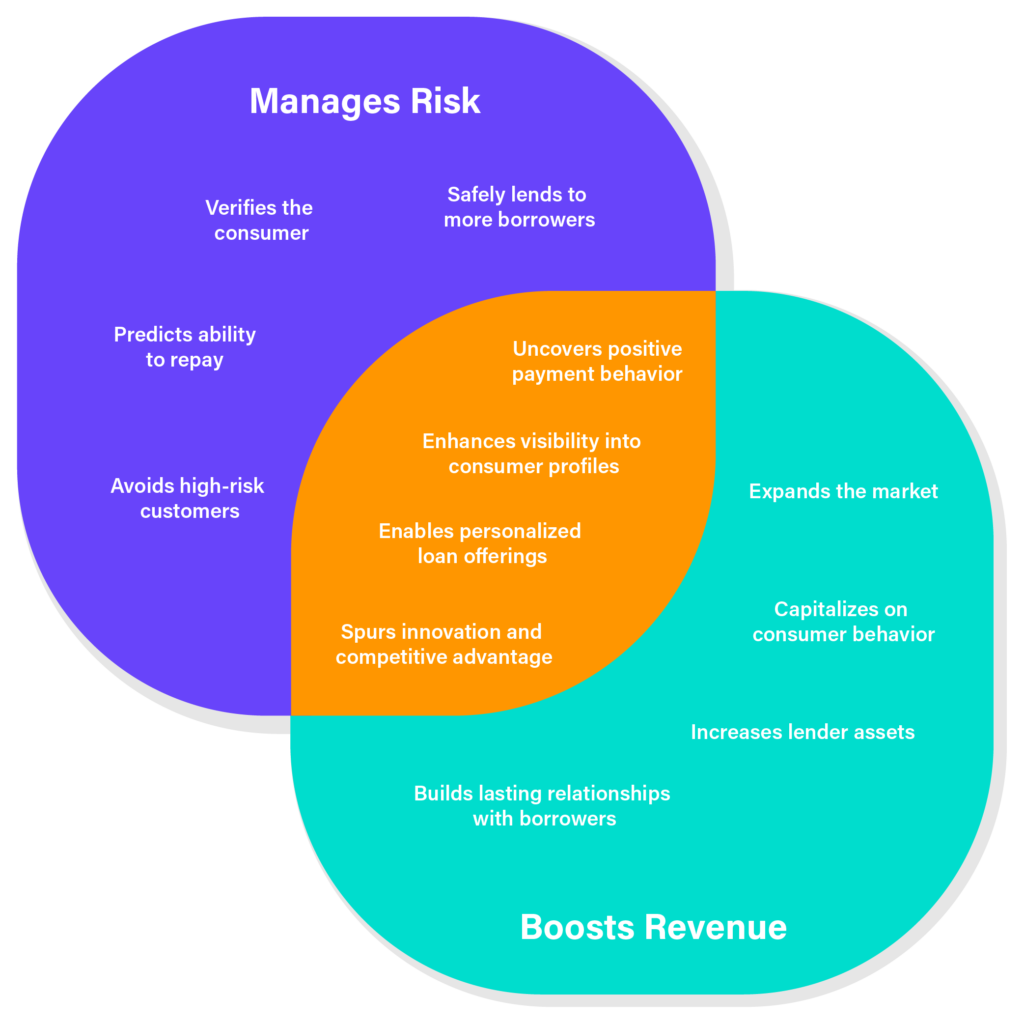

People often look at alternative data as a risk management tool. But the reality of its benefits is more complex; alternative data has the potential both to enhance risk assessment and boost revenue growth, across the organization. Let’s take a closer look at how this risk and revenue resource interacts with a lender day to day.

Advanced alternative credit scoring models could help extend credit to roughly 7.6 million consumers who are currently unscorable. So, why should lenders keep turning away potentially qualified applicants? And more importantly, what benefits are they missing out on from alternative data as a risk and revenue resource?

Alternative data: a tool for assessing risk

When you dive into it, alternative data can reduce lending risk in a few different ways. First and foremost, it enables lenders to quickly identify high-risk borrowers. Just like more traditional credit scoring models and sources, alternative data provides clear visibility into missed payments and transactions.

Secondly, new credit data can give lenders a clearer overall picture of the borrower, including verifying their identity and most recent transactions. As the Consumer Credit Reporting Reform Act alluded to, traditional credit bureau data is often at risk of becoming outdated or incomplete. Some forms of alternative data, on the other hand, are pulled in real time and on demand, providing recent and accurate payment data that lenders can trust. Likewise, alternative data sources can confirm existing data on consumers’ name and current address.

Wondering how to compare the various types of alternative credit data in the market? Check out our guide.

It’s also important to note: alternative data isn’t just an excuse to recklessly extend credit to subprime borrowers. It’s a tool to uncover and target the creditworthy applicants out of that pool. No one wants a repeat of 2008. Relying on the right alternative data sources – with proven predictive accuracy – will enable lenders to safely extend credit to the right borrowers.

Alternative data: a tool for growing revenue

On the flip side, alternative data also has exciting potential to help lenders tap into new and immense revenue opportunities. The numbers speak for themselves: nearly 50 million consumers in the U.S. are unbanked or underbanked. Approximately 160 million small businesses struggle to get off the ground, without viable loan options. Globally, 1.7 billion adults are still unbanked. Altogether, they add up to a vast market.

Bringing unbanked adults and businesses into the formal banking sector could generate nearly $380 billion in new revenues.

Meanwhile, as the competition between banks and fintechs gets more fierce to reach this market, advanced data analytics can help both gain an edge. PayPal, for instance, assesses annual transaction volume made through PayPal, then offers working capital accordingly, with no credit check. With the use of alternative data, lenders can become more nimble and offer new loan products to qualified customers faster than waiting on traditional models.

Once lenders capture these newly qualified applicants, they can also use alternative data to keep them. Only eight percent of Gen X is likely to remain loyal to their financial services providers after they have a negative interaction. Using the added visibility into spending behavior and patterns that alternative data can provide, lenders can build tailored products, offered at the right times, to keep borrowers enticed for a lasting relationship.

So, risk or revenue? Why not both?

Alternative data doesn’t only benefit risk and revenue in different ways: it benefits the entire organization. A more well-rounded understanding of the borrower and their spending behavior (positive or negative), is only ever useful to financial institutions.

And, once lenders better understand the borrower, they can tailor loan terms to meet what the consumer or business is prepared to afford. Customized loans ensure success in repayment – lowering the risk of default and improving chances of returns.

Alternative credit scoring is looking more and more like a credit scoring arms race.

Let’s not forget: alternative data is still relatively new to the market. Being one of the first to fully take advantage of it empowers risk professionals to expand their horizons with cutting-edge models. It doesn’t hurt for revenue either – alternative credit scoring is looking more and more like an arms race. As credit expert John Ulzheimer said: “It’s not like there’s a million prime consumers hiding under a rock somewhere.” Lenders who get to this market first will be ahead of the game.

Putting a viable risk and revenue resource into action

To take a step back, though, none of these benefits will be realized without putting ideas into action. There’s plenty at stake: this powerful new risk and revenue resource is lying in wait, to enhance risk assessment, generate personalized products, tap into new revenue streams, and more. Lenders only need to access it.

Ready to start exploring alternative data for your credit scoring models, but not sure where to begin? Check out our brief to learn how utility and telecom data can power your credit risk decisioning today.

You may also be interested in:

- Survey: Consumer Sentiments on Alternative Data Sharing

- 3 Ways to Assess Credit Risk with Utility Payment Data

- A Comprehensive Guide to Alternative Data Sources

If you like what you’re reading, why not subscribe?

About Amy Hou

Amy Hou is a Marketing Manager at Urjanet, overseeing content and communications. She enjoys writing about the latest industry updates in sustainability, energy efficiency, and data innovation.